{kind=link}

The National Association of Realtors (NAR) reported that the first-time home buyer share fell to a historic low of just 24%.

That was down from 32% a year earlier based on transactions between July 2023 and June 2024.

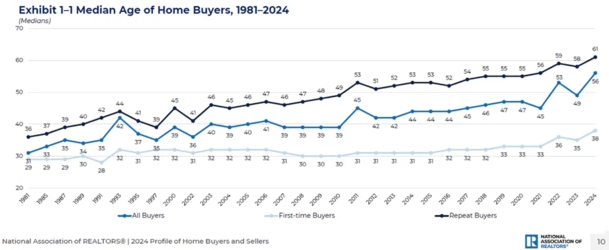

At the same time, the typical home buyer age reached an all-time high of 56 years old.

This all speaks to a housing market that has becoming increasingly unaffordable, especially for renters and young people.

But there is a silver lining; we aren’t seeing a flood of questionable home purchases as we did in the early 2000s.

Improved Underwriting Standards Prevent Risky Home Sales

I’ll start by saying the data is clearly negative.

Those statistics from NAR certainly don’t paint a pretty picture for the housing market at the moment.

The FTHB share hit a record low 24% in 2024, going all the way back to 1981. And it’s well below the historic norm of 40% prior to 2008.

It’s a sign that homes have become unaffordable for most, especially those who have never owned one before.

Without a large amount of sales proceeds (think repeat home buyers), it’s difficult to come up with the necessary down payment.

And without a big salary, it’s near-impossible to afford the monthly payment at today’s prices.

So obviously not great if you’re a young person or a renter without a parent willing to gift you a down payment. Or co-sign your mortgage.

Contrast that to the early 2000s when we had similar conditions in terms of housing affordability.

Back then, instead of home sales slowing, they kept rising thanks to things like stated income loans, and pay option ARMs.

So while we can sit here and complain about affordability, we could also arguably be happy that home sales have slowed at a time when purchasing them might not be ideal.

Sure, it’s not great for those who work in the industry nor prospective home buyers, especially first-time home buyers.

But it would be even worse if sales kept chugging along when perhaps they shouldn’t.

Imagine If We Just Kept Approving Everyone for a Mortgage

While fewer FTHBs are getting into homes, the typical age of home buyers has never been higher.

It increased to 56 years old for all buyers, 38 for FTHBs, and 56 for repeat buyers, all record highs!

In the early 2000s, we saw a ton of sales volume while home prices were close to their peak.

The reason home prices kept climbing and sales kept moving along was because exotic financing was pervasive.

Back then, you could get approved for a home loan with simply a credit score.

It didn’t matter if you couldn’t document your income or come up with a down payment. Or if you had no money in the bank.

And once you were approved, chances are they would give you an adjustable rate mortgage that wasn’t really affordable.

Or a 40-year mortgage or something else not sustainable or conducive to success as a homeowner. And after just a few months, there was a decent chance you’d already defaulted.

So from that point of view, it’s a healthy and natural reaction for home sales to slow.

If they kept on moving higher with affordability as bad as it is today, it’d be much more troubling. Instead, sales have been stopped in their tracks.

The Housing Market Is Naturally Resetting

All the data really tells us is that the housing market is resetting. And it’s a sign that either home prices need to ease. Or mortgage rates need to come down. Or wages need to increase.

Or perhaps a combination of all three.

It’s OK if we see a period of slowing home sales.

It tells us that something needs to change. That not all is well in the housing market. Or perhaps even the economy.

That’s arguably better than forcing home sales to continue with creative financing. And getting ourselves into the same mess we got into more than a decade ago.

I’m already reading about calls to bring back high-risk lending, including a proposal for a zero down FHA loan.

It’s already only a 3.5% minimum down payment, and they want to take it down to zero.

Maybe instead of that we need sellers to be more reasonable. Or perhaps we need more homes to be built.

But just forcing more sales with new forms of flexible financing seems like an all too familiar path we don’t want to go down again.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.