{kind=link}

I got active on Twitter over the past year and change and to my surprise (not sure why it’s surprising really), encountered lots of housing bears on the platform.

Many were/still are convinced that the next housing crash is right around the corner.

The reasons vary, whether it’s an Airbnbust, a high share of investor purchases, high mortgage rates, a lack of affordability, low home sales volume, rising inventory, etc. etc.

And the reasons seem to change as each year goes on, all without a housing crash…

So, now that we’re halfway through 2024, the obvious next question is will the housing market crash in 2025? Next year’s got to be the year, right?

But First, What Is a Housing Crash?

The phrase “housing crash” is a subjective one, with no real clear definition agreed to by all.

For some, it’s 2008 all over again. Cascading home price declines nationwide, millions of mortgage defaults, short sales, foreclosures, and so on.

For others, it might just be a sizable decline in home prices. But how much? And where?

Are we talking about national home prices or regional prices? A certain metro, state, or the nation at large?

Personally, I don’t think it’s a crash simply because home prices go down. Though it is a pretty uncommon occurrence to see nominal (non-inflation adjusted) prices fall.

Over the past few years, we’ve already experienced so-called home price corrections, where prices fell by 10%.

In 2022, we were apparently in a housing correction, defined as a drop in price of 10% or more, but not more than 20%.

Ostensibly, this means a drop of 20%+ is something much worse, perhaps a true housing crash.

But you have to look at the associated damage. If home prices fall 20% and there aren’t many distressed sales, is it still a crash?

Some might argue that there’s simply no other outcome if prices fall that much. And maybe they’d be right. The point is a crash needs to have major consequences.

If Homeowner Joe sells his home for $500,000 instead of $600,000, it’s not necessarily a disaster if he bought it for $300,000 a few years earlier.

He’s not happy about it, obviously, but it’s not a problem if he can still sell via traditional channels and even bank a tidy profit.

Of course, this means others who had to sell wouldn’t be so lucky, since their purchase price would likely be higher.

Still, this hinges on a major decline in prices, which historically is uncommon outside of the Global Financial Crisis (GFC).

Stop Comparing Now to 2008

One thing I see a lot is housing bears comparing today to 2008. It seems to be the go-to move in the doomer playbook.

I get it, it’s the most recent example and thus feels the most relevant. But if you weren’t there, and didn’t live it, you simply can’t understand it.

And if you weren’t, it’s hard to distinguish that time from now. But if you were, it’s clear as day.

There are myriad differences, even though they’re quick to mock those who say “this time is different.”

I could go on all day about it, but it’s best to focus on some main points.

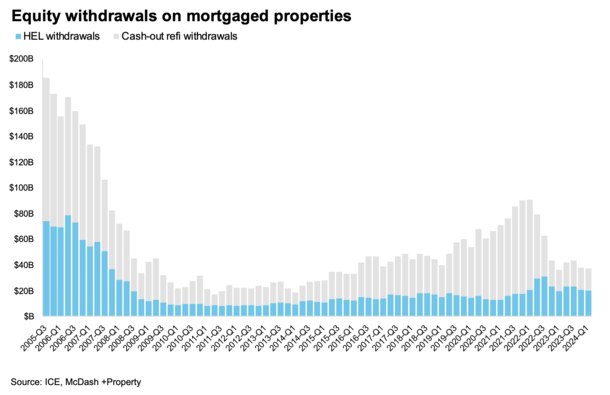

At the moment, housing affordability is poor thanks to a combination of high home prices and equally high mortgage rates, as seen in the chart above from ICE.

Despite a big rise in prices over the past decade, the high mortgage rates have done little to slow down the party.

Yes, the rate of home price appreciation has slowed, but given the fact that mortgage rates rose from sub-3% to 8% in less than two years, you’d expect a lot worse.

It’s just that there’s really no correlation between home prices and mortgage rates. They can go up together, down together, or move in opposite directions.

Now, proponents of a housing crash often point to buying conditions right now. It’s a horrible time to buy a house from a payment-to-income perspective. I don’t necessarily disagree (it’s very expensive).

But that completely ignores the existing homeowner pool. And by doing so, it’s a totally different thesis.

You can say it’s a bad time to buy but that the average homeowner is in great shape. These statements can coexist, even though everyone wants you to take one side or the other.

Look at the Entire Homeowner Universe

To put this perspective, consider the many millions of existing homeowners coupled with prospective home buyers.

Your average homeowner today has a 30-year fixed-rate mortgage set somewhere between 2-4%.

In addition, most purchased their properties prior to 2022, when home prices were a lot lower.

So your typical homeowner has a rock-bottom interest rate and a relatively small loan amount, collectively a very attractive monthly payment.

To make matters even better for the foundation of the housing market, which is existing homeowners, most have very low loan-to-value ratios (LTVs).

They’ve also got boring old 30-year fixed-rate loans, not option ARMs or some other crazy loan program that wasn’t sustainable, as we found out quickly in 2008.

These homeowners also haven’t tapped their equity nearly as much as homeowners did in the early 2000s, despite home equity being at record high levels (see above).

This is partially because banks and mortgage lenders are a lot stricter today. And partially because of mortgage rate lock-in. They don’t want to give up their low mortgage rate.

In other words, the low mortgage rate not only makes their payment cheap, it also deters taking on more debt! And more of each payment pays down principal. So these loans (and their borrowers) become less and less risky.

Some have turned to home equity loans and HELOCs, but again, these loans are much more restrictive, typically maxing out at 80% combined loan-to-value (CLTV).

In 2006, your typical homeowner did a cash-out refinance to 100% CLTV (no equity left!) while new home buyers were coming in with zero down payment as home prices hit record highs.

Take a moment to think about that. If that’s not bad enough, consider the mortgage underwriting at that time. Stated income, no doc, you name it.

So you had virtually all homeowners fully levered along with a complete lack of sound underwriting.

Slumping Home Sales in the Face of Poor Affordability Is Actually Healthy

That brings us to home sales, which have slumped since the high mortgage rates took hold. This is normal because reduced affordability leads to fewer transactions.

The worry is when this happens supply could outpace demand, resulting in home price declines.

Instead, we’ve seen low demand meet low supply in most metros, resulting in rising home prices, albeit at a slower clip.

While housing bears might argue that falling volume signals a crash, it’s really just evidence that it’s hard to afford a home today.

And the same shenanigans seen in the early 2000s to stretch into a home you can’t afford don’t fly anymore. You actually need to be properly qualified for a mortgage in 2024!

If lenders had the same risk tolerance they had back in 2006, the home sales would keep flowing in spite of 7-8% mortgage rates. And prices would move ever higher.

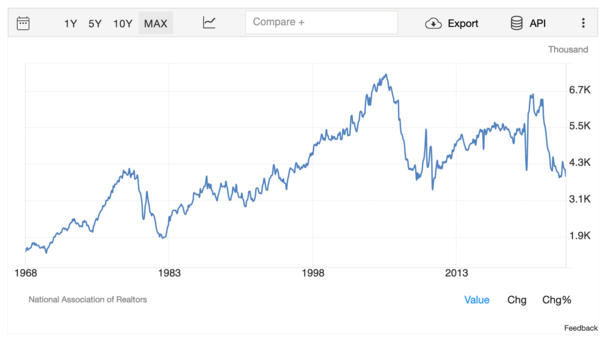

That spike in home sales in the early 2000s, seen in the chart above from Trading Economics, shouldn’t have happened. Fortunately, it’s not happening now.

At the same time, existing homeowners would be pulling cash out in droves, adding even more risk to an already risky housing market.

Instead, sales have slowed and prices have moderated in many markets. Meanwhile, existing owners are sitting tight and paying down their boring 30-year fixed mortgages.

And with any luck, we’ll see more balance between buyers and sellers in the housing market in 2025 and beyond.

More for-sale inventory at prices people can afford, without a crash due to toxic financing like what we saw in the prior cycle.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.