{kind=link}

Each year, an exciting new artificial intelligence (AI) investment seems to pop up. Sometimes these stocks flop after a year in the spotlight, and other times they continue to rise.

One newcomer in 2026 that I’m bullish on over the long term is Nebius (NBIS +3.30%), which gives clients everything they need to build, train, and run AI models and applications. Nebius has had an incredible year so far and has risen around 175% after five months.

But after looking at its prospects, I think the stock has a chance to move much higher this year, and just because you missed out on the initial run doesn’t mean you can’t cash in on future returns.

Image source: Getty Images.

Nebius is Nvidia-backed

Nebius is known as a neocloud company, a term that denotes businesses that are AI-focused, and Nebius is one of the best in this realm. Its platform has attracted both large and small clients, with businesses like Meta Platforms and Microsoft being prominent clients.

Today’s Change

(3.30%) $8.30

Current Price

$259.98

Key Data Points

Market Cap

$63B

Day’s Range

$234.75 – $264.41

52wk Range

$41.40 – $278.84

Volume

404.7K

Avg Vol

17.7M

Gross Margin

7.48%

Another key partner is Nvidia. It’s a significant investor in Nebius and gives it early access to new technology, making it a way for clients to use state-of-the-art computing products first. That’s an important partner to have in its industry and helps affirm that Nebius is the real deal.

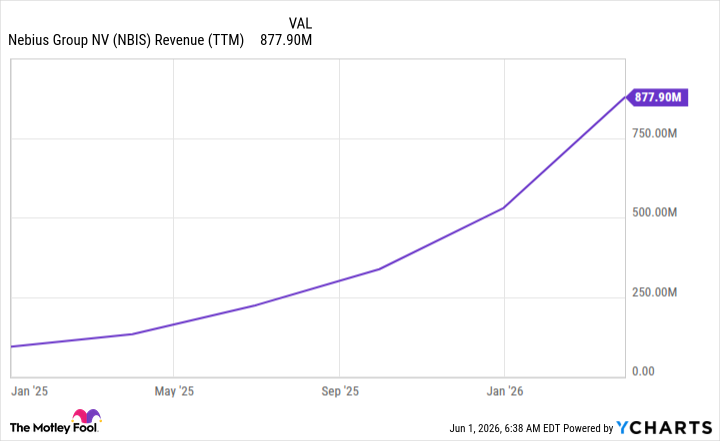

The company is undergoing rapid expansion to meet growing AI demand. In 2025, it had one data center site with 100-megawatt (MW) or greater power consumption; now, it’s up to seven. It has huge growth projections, with the overall target being a $7 billion to $9 billion annual run rate, up from $1.25 billion at the end of 2025.

So far, it’s executing on that projection after a first quarter during which revenue rose 684% year over year. And that’s just the beginning.

NBIS Revenue (TTM) data by YCharts; TTM = trailing 12 months.

Wall Street analysts project revenue will rise to $11 billion by the end of 2027. That’s huge growth from current levels and might spark investor curiosity since the stock could return a similar level of growth. However, with Nebius trading at 5.3 times 2027 sales, there’s a lot of growth already baked into the stock price. And management is in a growth-at-all-costs mindset, and profitability is a long way away.

There are some risks with that investors must be aware of, but I think the possible reward is far higher. As a result, I think Nebius is a solid buy right now, but investors should keep exposure limited due to elevated risk.

Keithen Drury has positions in Meta Platforms, Microsoft, Nebius Group, and Nvidia. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.